Rewarding the foolish ...

chispa

11 years ago

Related Stories

REMODELING GUIDESThe Hidden Problems in Old Houses

Before snatching up an old home, get to know what you’re in for by understanding the potential horrors that lurk below the surface

Full Story

MATERIALSRaw Materials Revealed: Drywall Basics

Learn about the different sizes and types of this construction material for walls, plus which kinds work best for which rooms

Full Story

MOST POPULAR8 Questions to Ask Yourself Before Meeting With Your Designer

Thinking in advance about how you use your space will get your first design consultation off to its best start

Full Story

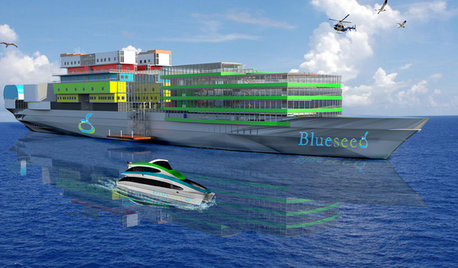

LIFECould Techies Get a Floating Home Near California?

International companies would catch a big business break, and the apartments could be cool. But what are the odds of success? Weigh in here

Full Story

DECORATING GUIDESDitch the Rules but Keep Some Tools

Be fearless, but follow some basic decorating strategies to achieve the best results

Full Story

LIFEYou Said It: ‘It’s Different ... But Then, Aren’t You?’ and More Wisdom

Highlights from the week include celebrating individuality and cutting ourselves some decorating slack

Full Story

BEFORE AND AFTERSSee 6 Yards Transformed by Losing Their Lawns

Wondering whether a turf lawn is the best use of your outdoor space? These homeowners did, and they found creative alternatives

Full Story

ARCHITECTUREGet a Perfectly Built Home the First Time Around

Yes, you can have a new build you’ll love right off the bat. Consider learning about yourself a bonus

Full Story

FLOORSDrama’s Afoot With Striking Black Floors

Be bold. Be brave. Drench your floors in black for a memorable interior scene

Full Story

BACKYARD IDEAS7 Backyard Sheds Built With Love

The Hardworking Home: Says one homeowner and shed builder, ‘I am amazed at the peace and joy I feel when working in my garden shed’

Full Story

sylviatexas1

EngineerChic

Related Professionals

Lafayette Architects & Building Designers · Eagan General Contractors · Delhi General Contractors · Hillsboro General Contractors · Mount Laurel General Contractors · Norfolk General Contractors · Parsons General Contractors · Reisterstown General Contractors · Roselle General Contractors · Rossmoor General Contractors · Salem General Contractors · Avenal General Contractors · Kennesaw Home Stagers · McLean Home Stagers · Ogden Interior Designers & DecoratorschispaOriginal Author

gmp3

brickeyee

sylviatexas1

brickeyee

gmp3

EngineerChic

chispaOriginal Author

EngineerChic

graywings123

brickeyee

gmp3

User

sas95

EngineerChic

gmp3

EngineerChic

weedyacres

sylviatexas1

brickeyee

sylviatexas1

brickeyee

chispaOriginal Author

sylviatexas1

gmp3

gmp3

chispaOriginal Author