House Price to Income Ratio?

leafy02

14 years ago

Sort by:Oldest

Comments (10)

Related Stories

REMODELING GUIDESDesign Workshop: Is an In-Law Unit Right for Your Property?

ADUs can alleviate suburban sprawl, add rental income for homeowners, create affordable housing and much more

Full Story

HOUZZ TOURSHouzz Tour: A Portland Bungalow Gets a Major Lift

Raising a whole house allowed 5 extra bedrooms and a walk-out basement — plus a boost in income

Full Story

LIFECould You Be a Landlord?

Sure, the extra income would be great. But jumping blindly into owning a rental property could be disastrous. Here's what you need to know

Full Story

DECORATING GUIDESThe Secret Formula for Perfect Pillow Arrangements

For a polished look on sofas and beds every time, keep this simple ratio for pillow arranging in mind

Full Story

SMALL HOMESHouzz Tour: Sustainable, Comfy Living in 196 Square Feet

Solar panels, ship-inspired features and minimal possessions make this tiny Washington home kind to the earth and cozy for the owners

Full Story

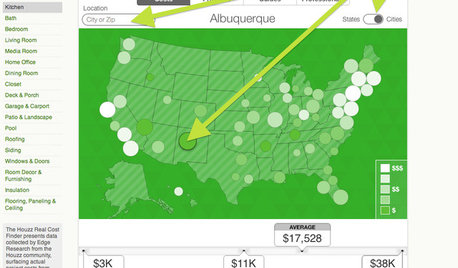

REMODELING GUIDESBreakthrough Budgeting Info: The Houzz Real Cost Finder Is Here

Get remodeling and product prices by project and U.S. city, with our easy-to-use interactive tool

Full Story

DIY PROJECTSReinvent It: Salvage Savvy Keeps an Urban-Farmhouse Bath on Budget

See how resourceful shopping and repurposing gave a homeowner the new bathroom she wanted at the right price

Full Story

VACATION HOMESMake Your Vacation Home Pay Off

Renting your vacation house when you're not using it makes good financial sense. These tips can help

Full Story

GARDENING AND LANDSCAPINGChoosing a Deck: Plastic or Wood?

Get the pros and cons of wood, plastic, composite and more decking materials, plus a basic price comparison

Full Story

DESIGN PRACTICEDesign Practice: How to Pick the Right Drawing Software

Learn about 2D and 3D drawing tools, including pros, cons and pricing — and what to do if you’re on the fence

Full StoryMore Discussions

susanjn

emilynewhome

Related Professionals

Winchester Architects & Building Designers · Town and Country Architects & Building Designers · Abington General Contractors · Brighton General Contractors · Claremont General Contractors · Milton General Contractors · North Lauderdale General Contractors · Redan General Contractors · Tamarac General Contractors · Tyler General Contractors · Kearny Home Stagers · Lynn Home Stagers · South Miami Heights Home Stagers · Nashville Interior Designers & Decorators · Wareham Interior Designers & Decoratorsleafy02Original Author

calliope

clemrick

chrisk327

Billl

worthy

brickeyee

eal51