budgeting if varied monthly income

lbelle

17 years ago

Sort by:Oldest

Comments (6)

Related Stories

FEEL-GOOD HOMESimple Pleasures: 10 Ideas for a Buy-Less Month

Save money without feeling pinched by taking advantage of free resources and your own ingenuity

Full Story

KITCHEN DESIGN15 Farmhouse Kitchens That Made Us Swoon This Month

Raw wood, natural light, shiplap siding — we just couldn’t get enough of these farmhouse-style kitchens uploaded to Houzz in January

Full Story

DIY PROJECTSReinvent It: Salvage Savvy Keeps an Urban-Farmhouse Bath on Budget

See how resourceful shopping and repurposing gave a homeowner the new bathroom she wanted at the right price

Full Story

KITCHEN DESIGNKitchen Remodel Costs: 3 Budgets, 3 Kitchens

What you can expect from a kitchen remodel with a budget from $20,000 to $100,000

Full Story

DECORATING GUIDESCreate a Chic First Apartment on a Dorm Room Budget

Show your first solo place off with pride by incorporating these tips for budget-friendly artwork, furniture and accessories

Full Story

REMODELING GUIDESWhat to Know About Budgeting for Your Home Remodel

Plan early and be realistic to pull off a home construction project smoothly

Full Story

REMODELING GUIDES8 Ways to Stick to Your Budget When Remodeling or Adding On

Know thyself, plan well and beware of ‘scope creep’

Full Story

DECORATING GUIDESBudget Decorator: Let’s Go Thrifting

Dip into the treasure trove of secondhand pieces for decor that shows your resourcefulness as much as your personality

Full Story

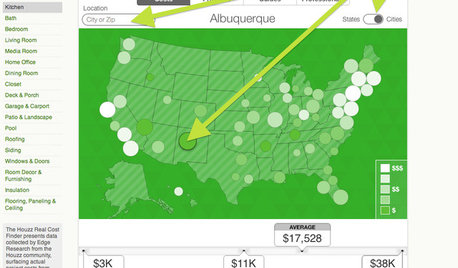

REMODELING GUIDESBreakthrough Budgeting Info: The Houzz Real Cost Finder Is Here

Get remodeling and product prices by project and U.S. city, with our easy-to-use interactive tool

Full Story

DECORATING GUIDESBudget Decorator: How to Save When You Don’t DIY

You don’t have to be crafty to decorate your home inexpensively. Here are other ways to stretch your design dollars

Full StorySponsored

More Discussions

joyfulguy

qdognj

Related Discussions

monthly cost of waterfalls??

Q

House Price to Income Ratio?

Q

If you're getting by on a thin income ...

Q

Need More 'Ants' -- And Higher-Income Jobs

Q

User

lbelleOriginal Author

qdognj

steve_o