New user! Beginning Steps - Survey, Loans, Design

thecatsmeowth

11 years ago

Related Stories

INSIDE HOUZZHouzz Survey: See the Latest Benchmarks on Remodeling Costs and More

The annual Houzz & Home survey reveals what you can expect to pay for a renovation project and how long it may take

Full Story

INSIDE HOUZZThere’s a Party in the Backyard, Says a Houzz Landscaping Survey

Entertaining, growing edibles and solving problems are goals for homeowners planning to revamp their yards

Full Story

GARDENING AND LANDSCAPINGHouzz Survey: See What Homeowners Are Doing With Their Landscapes Now

Homeowners are busy putting in low-maintenance landscapes designed for outdoor living, according to the 2015 Houzz landscaping survey

Full Story

INSIDE HOUZZA New Houzz Survey Reveals What You Really Want in Your Kitchen

Discover what Houzzers are planning for their new kitchens and which features are falling off the design radar

Full Story

REMODELING GUIDESHouzz Survey: Renovations Are Up in 2013

Home improvement projects are on the rise, with kitchens and baths still topping the popularity chart

Full Story

REMODELING GUIDESHouzz Survey Results: Remodeling Likely to Trump Selling in 2014

Most homeowners say they’re staying put for now, and investing in features to help them live better and love their homes more

Full Story

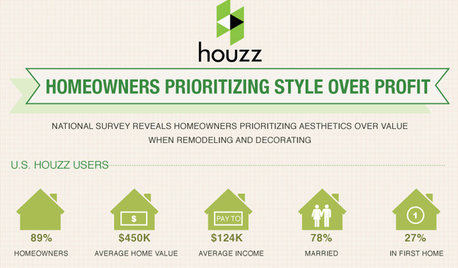

Houzz Survey: Livability Trumps Home Value

Increasing home value comes in a distant second among those planning home improvements. Many plan to do some of the work themselves

Full StoryREMODELING GUIDESBathroom Remodel Insight: A Houzz Survey Reveals Homeowners’ Plans

Tub or shower? What finish for your fixtures? Find out what bathroom features are popular — and the differences by age group

Full Story

FUN HOUZZSurvey Says: We’re Scared of Being Home Alone — and Spiders

A new Houzz survey reveals that most of us get spooked in an empty house. Find out what’s causing the heebie-jeebies

Full Story

STUDIOS AND WORKSHOPSCreative Houzz Users Share Their ‘She Sheds’

Much thought, creativity and love goes into creating small places of your own

Full Story

CamG

User

Related Professionals

Pedley Architects & Building Designers · Plainfield Architects & Building Designers · Ellicott City Home Builders · Jurupa Valley Home Builders · Puyallup Home Builders · The Colony Home Builders · Warrensville Heights Home Builders · Stanford Home Builders · Brownsville General Contractors · Jacksonville General Contractors · Rolling Hills Estates General Contractors · Shaker Heights General Contractors · Stoughton General Contractors · Tabernacle General Contractors · Waxahachie General Contractorsdekeoboe

thecatsmeowthOriginal Author